And Why Decaf Is Building the Infrastructure

Maria runs a small business from Caracas. She handles customer support and operations for startups in the United States, earning around $800 a month — real money in a country where the average salary is a fraction of that. The work is fine. Getting paid is the problem. Her clients send payments through PayPal or similar platforms. The money shows up in her account — technically. But withdrawing it? That's another story. Days of waiting. Fees layered on top of fees. Currency conversion losses. Sometimes her funds get flagged for review with no explanation and no timeline. When you're living paycheck to paycheck, "your money is available in 3–5 business days" isn't an inconvenience. It's a crisis. Maria's story isn't unusual. It's the norm for tens of millions of people.

The Global Workforce Is Growing. Payments Are Still Stuck in 1995.

There are roughly 180 million remote workers worldwide today, and that number keeps climbing. They write code, moderate content, label AI training data, support customers, create content — all for companies thousands of miles away. The work is digital. Instant. Global. The payment infrastructure is not. Workers routinely lose 10–20% of their earnings to fees, conversion losses, and settlement delays. The biggest financial risk for most online workers isn't market volatility — it's waiting two weeks for their own money to clear. Legacy payment systems were designed for a world that no longer exists.

Stablecoins Cracked the First Half of the Problem

Blockchain-based stablecoins — USDC, USDT — are genuinely transformative infrastructure. They move money globally in seconds, at a fraction of a cent, without touching traditional banking rails. For the sender — a payroll platform, a marketplace, a startup paying contractors — stablecoins are close to perfect. The hard part of cross-border payments (moving value across borders quickly and cheaply) is essentially solved. The hard part that remains is on the other end. A worker in Venezuela or Colombia or Nigeria receiving USDC still needs to pay rent. Buy groceries. Send money to their parents. Withdraw local currency. Receiving stablecoins is only useful if you can actually spend them — and for most of the world, that last step is still broken. This is the last-mile problem. It's where most "modern" payment systems still fall apart.

Messaging Is Already the Internet for Most of the World

While payments were evolving, something else happened quietly: messaging apps became the primary interface for the internet. WhatsApp has 2.7 billion users. In Latin America, Southeast Asia, and Sub-Saharan Africa, it's not just an app — it's how people communicate, run businesses, coordinate deliveries, and stay connected with family. For billions of people, if something isn't on WhatsApp, it effectively doesn't exist. The question isn't whether messaging will become a payment channel. It already is — informally, imperfectly, everywhere. The question is who builds the infrastructure to make it work properly.

That's what Decaf is building.

What It Looks Like in Practice

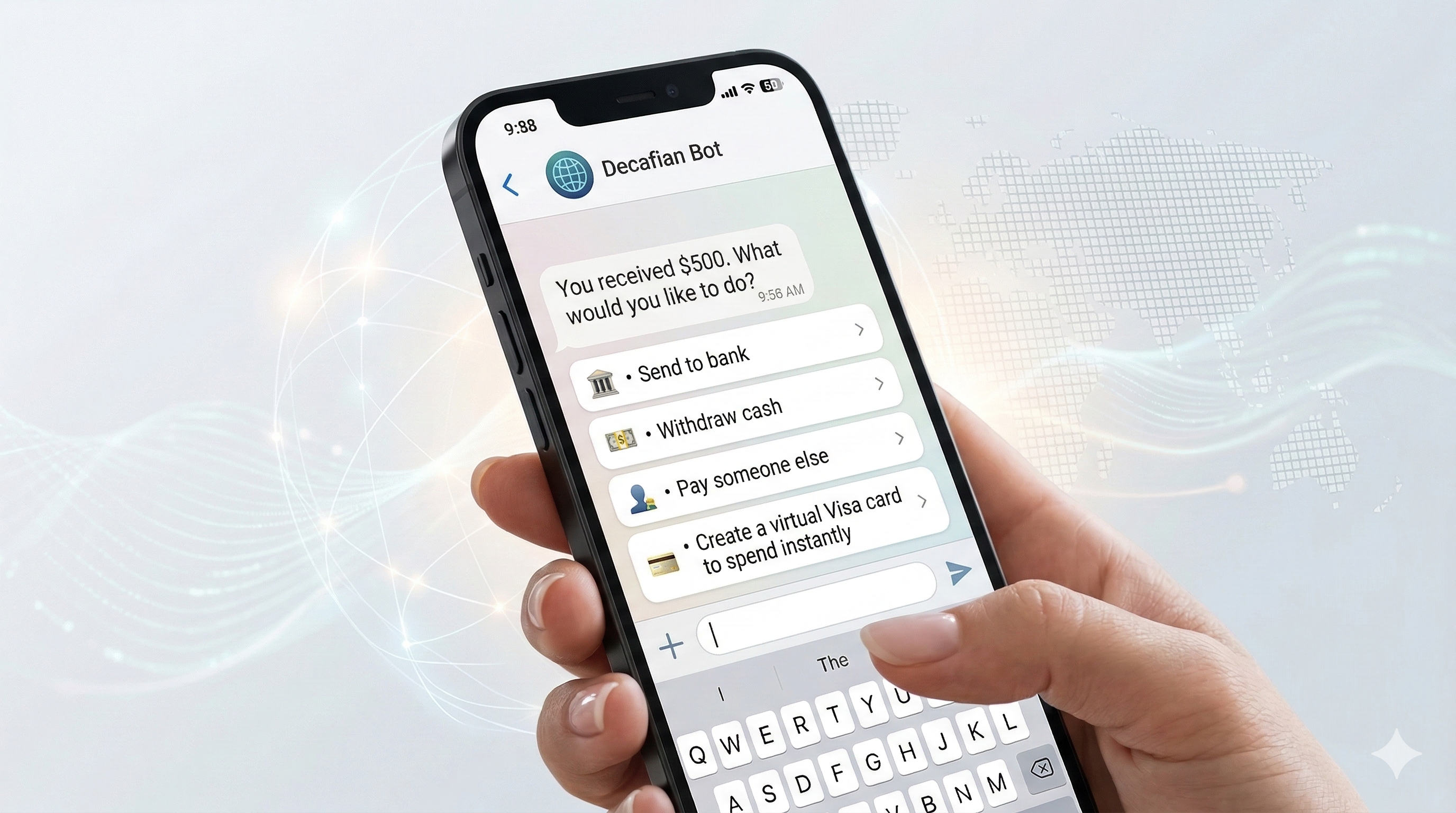

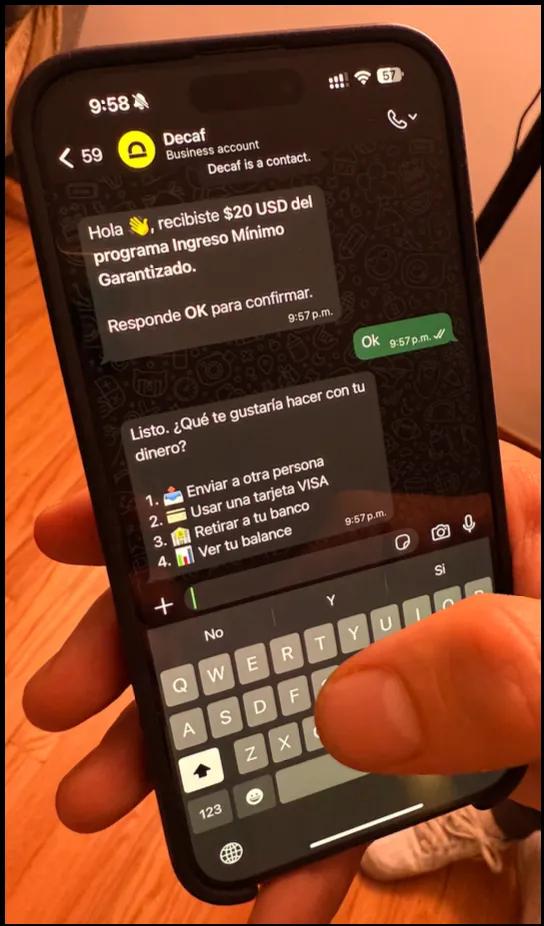

Imagine your phone buzzes. A WhatsApp message:

You received $500 from Acme Corp. What would you like to do? → Send to bank account → Withdraw cash → Pay someone → Keep as digital dollars → Earn Yield/Invest → Get a Visa card

That's it. No app to download. No account to create. No KYC maze to navigate. You reply, and your money moves. This is what messaging-native payments look like. Not a fintech app that happens to send notifications — a financial system that lives natively inside the messaging platform you're already using.

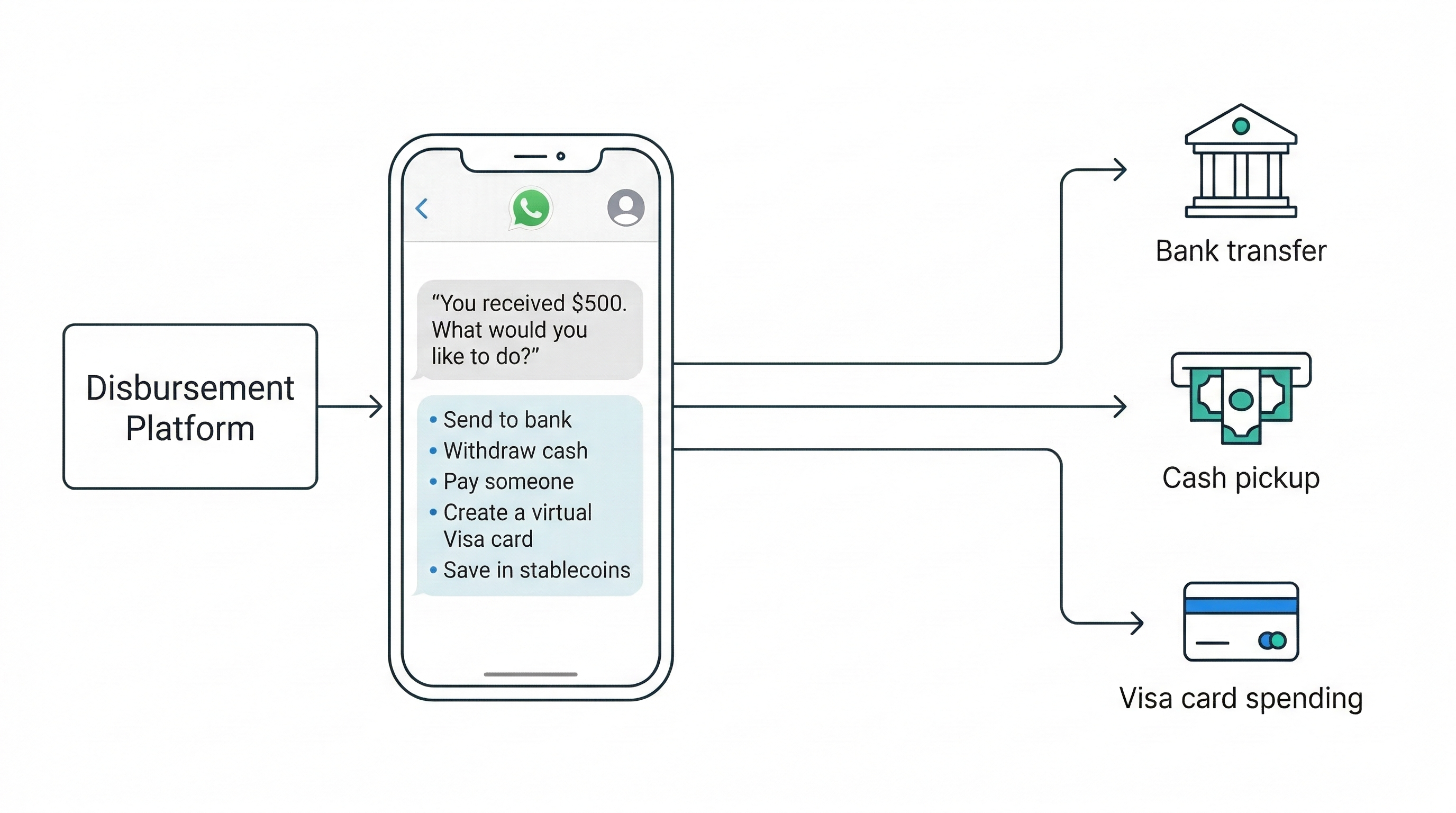

The Decaf Infrastructure

Behind that simple WhatsApp message is serious infrastructure. Decaf connects stablecoin settlement with real-world financial rails across 180+ countries. When someone receives money through Decaf, they can: • Bank transfer - direct to local bank accounts in USD, EUR, MXN, COP, BRL, and more • Cash pickup - through MoneyGram's network in 186 countries • Visa card - virtual or physical, usable anywhere Visa is accepted • Send to anyone - forward funds to another phone number instantly • Earn Yield/Invest - buy tokenized equities, bonds, and commodities Blockchain handles settlement on the backend. Users never see it. They just see a message and a choice.

Built for Platforms, Not Just Individuals

Decaf isn't just a consumer wallet. It's infrastructure for any organization that moves money to people at scale. A single API call is all it takes:

decaf.pay( phone="+573001234567",

email="maria@example.com", amount=500, currency="USD" ) The recipient gets a WhatsApp message. They choose what to do with the money. Done. This works for: • Freelance and creator platforms paying talent across LATAM, Africa, and Southeast Asia • Gig economy companies disbursing to drivers and couriers without bank accounts • Humanitarian organizations distributing aid directly to recipients' phones • Remote-work platforms running global payroll without the complexity of traditional wire transfers • AI workflows making micro-payments to human contributors in real time For the sender: one API, one call, global reach. For the recipient: a message, a choice, immediate access.

The Market Is Enormous. The Infrastructure Doesn't Exist Yet.

Remittances alone exceed $700 billion annually. Cross-border payroll, creator payouts, and humanitarian cash transfers add hundreds of billions more. Across all of it, the problem is the same: money moves too slowly, costs too much, and excludes too many people. Stablecoins solved the settlement layer. Messaging solves the access layer. What's missing is infrastructure that connects them — infrastructure that works for the people actually receiving the money, not just the platforms sending it. That's what Decaf is building. The future of global payments isn't another app. It's the message you already got.